Miscategorizing transactions is one of the most common yet dangerous bookkeeping errors small business owners commit. For instance, imagine this: Alex and Jordan own a thriving craft brewery that’s expanding rapidly. Additionally, they’re partners in a separate restaurant group that operates a taproom featuring their beers—a natural synergy.

Consequently, the brewery often transfers funds to the restaurant side to cover equipment upgrades, inventory shortfalls, or seasonal cash crunches. These transfers are sometimes informal “advances,” sometimes documented loans, and occasionally structured as contractual investments tied to future revenue shares.

In their accounting software, Alex handles most of the bookkeeping. Every transaction gets recorded promptly, nothing sits in “uncategorized,” and bank feeds are reconciled weekly. “We’re on top of it,” Alex assures Jordan. “As long as the money is tracked somewhere, the exact category doesn’t matter that much.”

However, here’s what’s really happening when miscategorizing transactions occurs:

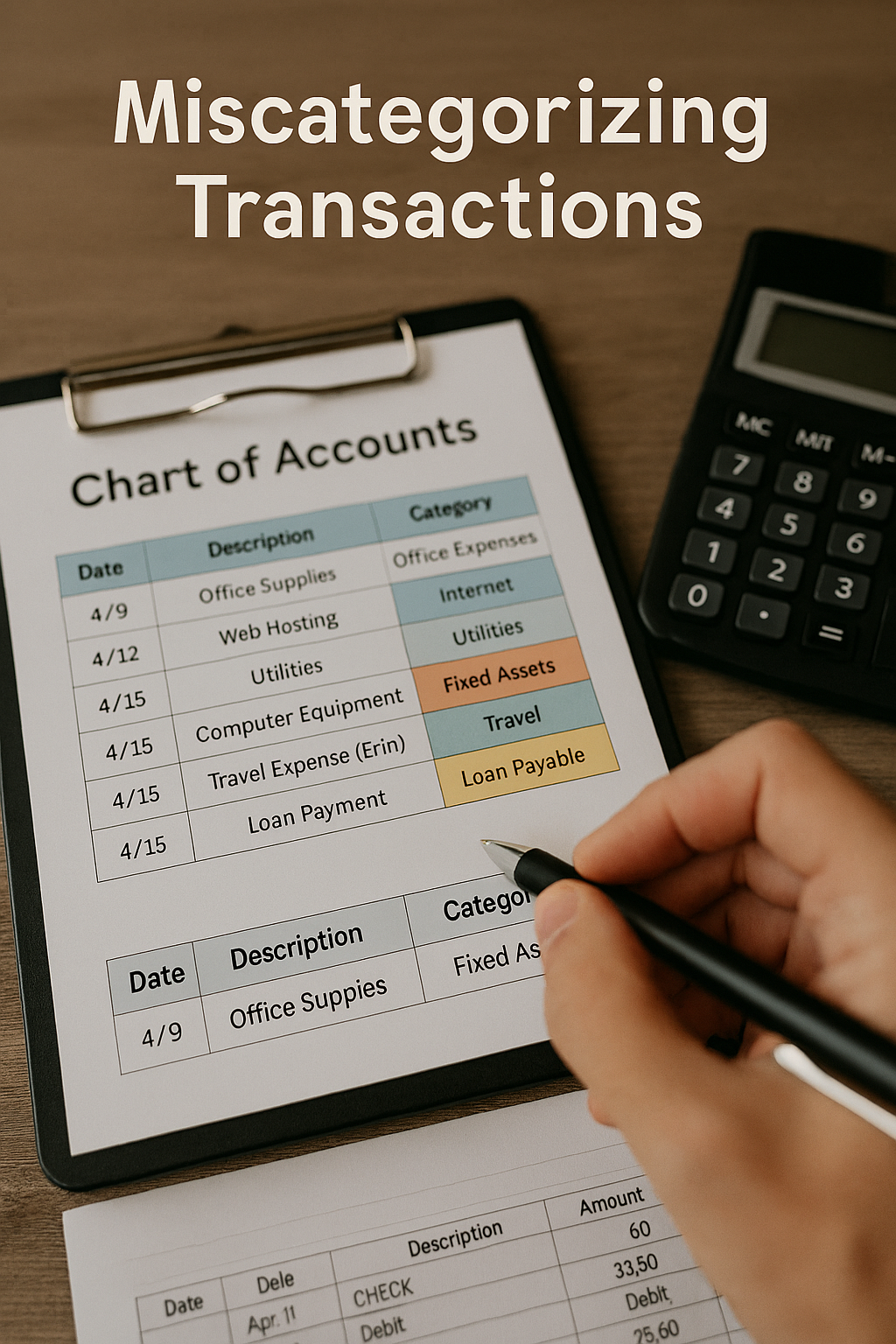

- Transfers to the restaurant business—whether true loans, repayable advances, or contractual investments—are routinely coded as expenses like “contract labor,” “marketing,” or “professional services.”

- Bulk purchases of hops, malt, and packaging materials (direct Cost of Goods Sold) get categorized as general “supplies” or “operating expenses.”

- The new $12,000 brewing tank is expensed immediately rather than capitalized and depreciated.

- Principal repayments on the brewery’s equipment loan are lumped in with “interest expense.”

- Occasional personal meals or travel slip through as “business development.”

As a result, Alex and Jordan believe they’re being diligent. In reality, miscategorizing transactions like these creates distortions that could unravel everything when they start pitching investors for the next phase of growth.

Moreover, these kinds of miscategorizations are incredibly common in small and mid-sized businesses—especially those with related entities or partner ventures—and every single one is equally dangerous.

Breaking Down the Most Common Miscategorization Mistakes

First, no error stands out as “worse” than the others. Instead, they all erode the reliability of your financial statements in interconnected ways:

- Transfers to a partner or related business recorded as expenses Whether they’re loans, repayable advances, or contractual investments, these outflows should appear as assets (loans receivable or investments) on your balance sheet—not as deductible expenses. Therefore, miscategorizing transactions here permanently inflates costs and hides money owed back to the company. The IRS closely scrutinizes related-party transactions for proper treatment. Learn how related party transactions can trigger the IRS scrutiny here.

- Inventory or COGS purchases recorded as operating expenses This understates true Cost of Goods Sold, artificially boosting gross margins and making profitability look stronger (or weaker) than reality. In addition, proper separation is key for accurate reporting. This resource provides a detailed explanation of how to differentiate cost of goods sold from operating expenses and determine the appropriate classification for each transaction: Fondo.

- Major equipment or asset purchases expensed immediately Instead of capitalizing and depreciating over time, the full cost hits the current year, overstating expenses and leaving assets off the balance sheet.

- Principal portions of loan repayments treated as deductible expenses Only interest is deductible; therefore, misclassifying principal creates improper deductions.

- Personal expenses mixed into business categories This risks full disallowance during an audit and undermines professional credibility.

In summary, each of these shifts items improperly between expenses, assets, and liabilities, turning what should be clear financial statements into misleading fiction.

The Real Damage These Errors Cause

1. A Completely Distorted Financial Picture

To begin with, Profit & Loss statements can swing wildly depending on the mix of errors. Consequently, gross margins become unreliable. Furthermore, the balance sheet misses key assets—like money owed from a partner business or capitalized equipment—while liabilities may be misstated. As a result, metrics such as EBITDA, working capital, and debt ratios lose all meaning.

2. Serious Tax Risks

Many owners quietly think, “Higher expenses mean lower taxable income—that’s smart, right?” However, it’s a pervasive and dangerous myth. When those inflated expenses include non-deductible items—loan principal, advances to related entities, capital assets, or contractual investments—you’re claiming deductions you don’t deserve. For example, an IRS audit can disallow them, resulting in back taxes, penalties, and interest. Conversely, failing to capitalize assets means missing legitimate depreciation deductions over multiple years.

3. Poor (or Impossible) Decision-Making

Next, you can’t accurately assess product-line profitability, control costs, or plan cash flow when fundamental categories are wrong. Thus, messy books hide the truth about whether partnerships are truly adding value.

4. Death by Due Diligence

Finally, investors, especially in businesses with related entities, scrutinize inter-company transactions intensely. When they discover miscategorizing transactions—such as expensing transfers to a partner business—they raise alarm bells. This could signal sloppy bookkeeping or worse, and it can kill a funding round instantly.

Why So Many Owners Fall Into the “Close Enough” Trap

On one hand, business owners are busy building products, serving customers, and driving revenue—bookkeeping precision often feels secondary. On the other hand, related-party transactions feel especially gray: “It’s all in the family (or partnership)—why overcomplicate it?”

In addition, the tempting but flawed belief that pumping up expenses saves taxes today leads to routine shortcuts. However, when outside capital is on the table, “close enough” turns into “not even in the ballpark.”

How to Fix It: Practical Steps to Clean, Accurate Books

Immediate Cleanup

- First, review recent transactions and reclassify systematically: move partner-business transfers to proper “Loans Receivable,” “Due from Related Party,” or “Investments” accounts; shift inventory to COGS; capitalize assets.

- Then, involve a CPA early—reclassifications, especially involving related entities, can have tax and legal implications.

Build a Strong Foundation

- Customize your chart of accounts with clear buckets for COGS, operating expenses, assets (including specific related-party receivable/investment accounts), liabilities, and equity.

- Additionally, document related-party transactions properly—use loan agreements, promissory notes, or investment contracts, even if simple.

Ongoing Habits for Accuracy

- Review automation rules regularly and spot-check categorizations.

- Reconcile monthly and maintain separate banking for each entity.

- Track depreciation schedules diligently.

Get Professional Help When Needed

Outsource bookkeeping or engage an accountant for reviews—particularly before investor discussions or when related-party transactions are frequent. Ultimately, the investment pays for itself in credibility and peace of mind.

Ready to Fix Your Books?

Miscategorizing transactions isn’t just a minor oversight—it distorts your financials, risks costly tax issues, and can scare away investors. However, the good news is that it’s fixable.

If you’re dealing with messy categorizations, inter-company loans, or cleanup before a big pitch, reach out to NYA Solutions LLC. We specialize in transaction cleanup, helping small businesses like yours get accurate, investor-ready books fast. Contact NYA Solutions LLC today for a consultation and take the first step toward clean, compliant financials.